Table Of Content

The exact amount you’ll qualify for will depend on your finances and vary from lender to lender. The best way to determine how much mortgage you can qualify for is to start the mortgage application process. While your lender is willing to loan you a substantial amount of money, that doesn’t mean you have to borrow the entire amount if it would put you under significant financial strain.

Calculate your buying power

Equally, the lower the interest rate you can get the less you’ll pay each month against your mortgage as well as over the life of the loan. Below are some hypothetical examples of how slight differences in your APR(%) can impact what you pay against your mortgage. There is something to be said for the idea of not maxing out your credit possibilities.

The Bankrate promise

As you determine how much house you can afford, remember to factor in down payments, especially if you’re trying to afford the 20% to avoid PMI. Note that you might not have to put down anything at all if you qualify for certain government loans. Take some of your extra money and put it toward your mortgage principal every month to pay off the loan faster. How large of a mortgage loan you can qualify for depends on how much debt a lender thinks you can take on as a borrower. This will ultimately determine how much house you’re able to afford. Get Forbes Advisor’s ratings of the best mortgage lenders, advice on where to find the lowest mortgage or refinance rates, and other tips for buying and selling real estate.

Explore homes with the Redfin app anytime, anywhere.

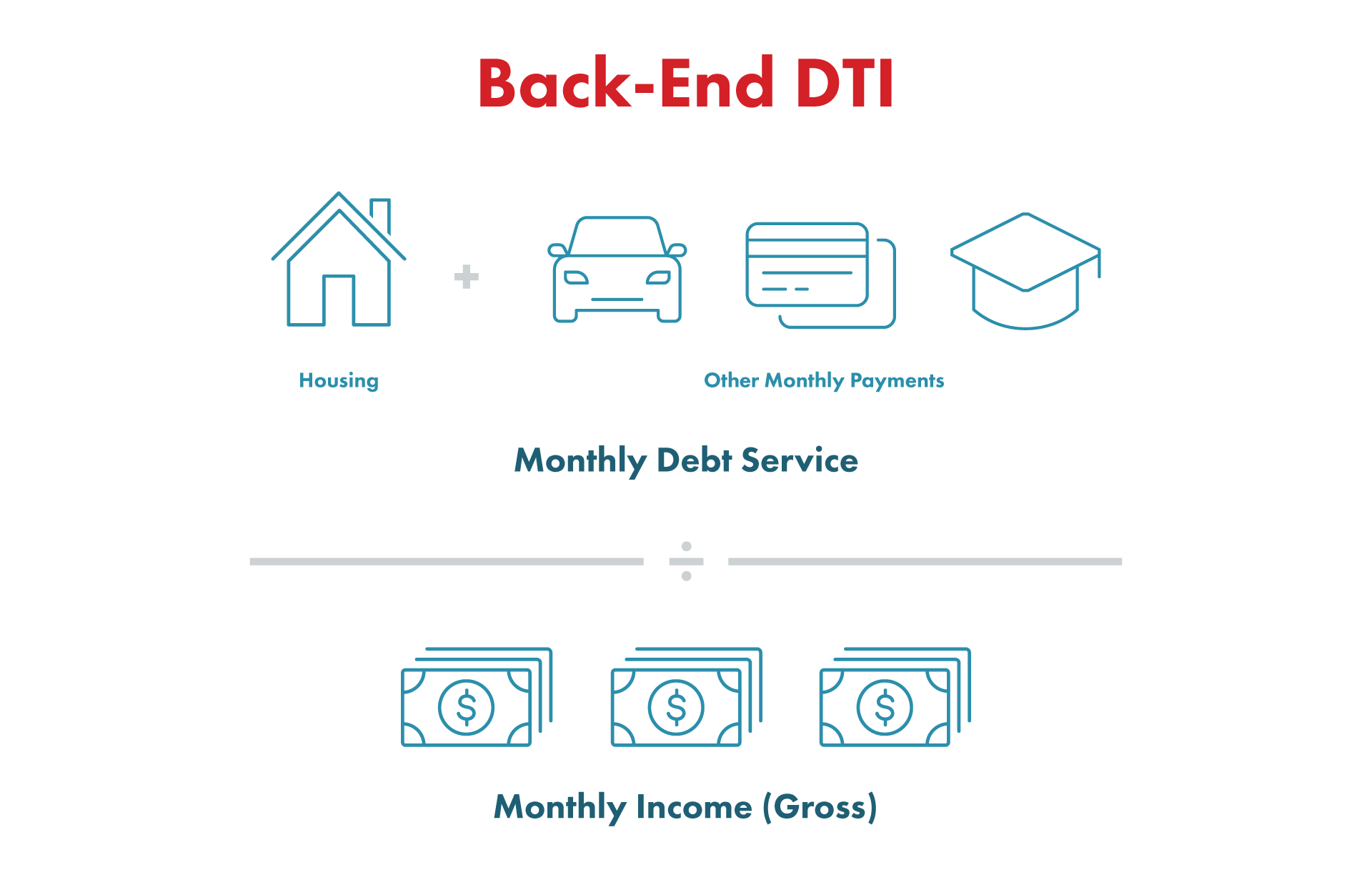

Also, if you already calculated all expenses on a house and get a certain number, say, $1,450, you should try and cut down your $600 monthly payments by $250 for a better chance at a loan. When you apply for a mortgage, your lender ideally will want to see a 2-year work history before they grant approval. If you choose to take the largest loan you qualify for, will you be able to make those higher monthly payments during a period of unemployment? Let’s say you still take out the $200,000 loan with a 5% interest rate, but the term is 30 years. Your monthly payments will now be $1,074 (excluding taxes and insurance). According to the 29/41 rule, you should spend no more than 29% of your gross income on housing and no more than 41% of your gross income on the sum of all debt payments, housing included.

Title insurance

While the maximum debt-to-income ratio is set at 41% in the general guidelines for VA loans, the VA backs loans for people with higher ratios provided they meet other requirements. VA loans don’t have credit score requirements (although the credit score will still affect the borrower’s interest rates) and borrowers can qualify for a 0% down payment. Before buying a home, you want to know how much house you can afford.

How much should I spend on a new home?

As a general trend, more rural U.S. states have lower costs compared with states home to numerous large cities, such as California and New York — especially when it comes to housing. The city is a melting pot of cultures, leading to a wide array of food, music, and festivals. Residents can enjoy cuisine from all over the world, visit museums like the Getty Center, or attend live shows and concerts. However, newcomers should be aware that traffic congestion is a significant issue, and public transportation options, while improving, may not cover all areas extensively.

#4: Explore all of your mortgage options

For example, if you realize you have $3,000 left over at the end of each month, decide how much of that could be allocated toward a mortgage. In the mortgage process, it’s important to look at your budget, savings and assets for a couple of reasons. Apply online for expert recommendations with real interest rates and payments. You might not want to borrow the maximum amount a lender offers you.

See what you can afford and find homes within your budget.

Assessing how much you should spend on a house requires a bit of a look into your current and potentially future financial situation. Before you take on the maximum loan you can get and start looking at more expensive houses, consider these tips. Suppose you bought the same $200,000 house as above with the 15-year fixed mortgage at 5% but the mortgage interest rate changed to 6.25%. If you have a VA loan, guaranteed by the Department of Veterans Affairs, you won’t have to put anything down or pay for mortgage insurance, but you will have to pay a funding fee. Loan requirements for cash reserves usually range from zero to six months. But even if your lender allows it, exhausting your savings on a down payment, moving expenses and fixing up your new place is tempting fate.

Mortgage Calculators

Add in all those other non-mortgage expenses and see what you’ll be spending each month. First, it’s important to check your credit report from all three bureaus — Experian, TransUnion and Equifax — for inaccuracies. If there are mistakes in your credit history, you can file a dispute with the credit agencies. There are several options to consider if you are struggling to afford the home you have your eyes on. Some methods must be undertaken over time, whereas others will immediately impact your mortgage application.

VA loans make home ownership more possible for borrowers than it otherwise would be through conventional mortgage loans, primarily because a VA loan does not require any down payment. Additionally, interest rates offered for VA loans often turn out to be lower than those offered for conventional loans. The back-end debt ratio includes everything in the front-end ratio dealing with housing costs, along with any accrued recurring monthly debt like car loans, student loans, and credit cards. As the cost of homebuying climbs, first-time buyers need a six-figure salary to purchase the average home. Research released Monday from real estate company Clever finds that with a 10% down payment, buyers need to earn nearly $120,000 to afford a median-priced home.

What it will take to make homes affordable again for millions of Americans - CNBC

What it will take to make homes affordable again for millions of Americans.

Posted: Wed, 25 Oct 2023 07:00:00 GMT [source]

The loan does not require any down payment, and unlike other loans, it also does not require private mortgage insurance. When you’re purchasing a home, whether you’re just getting started or in the final stages of a deal, it’s best to keep your finances in tip-top shape. This means not making any big purchases (like a new car) or running up the tab on your credit cards, both of which could impact your credit score.

The exact amount you should spend on a new home depends on your financial situation. Ideally, you’ll want to avoid spending more than a third of your gross monthly income on your mortgage. However, depending on your finances, you may be able to afford a slightly more expensive home.

No comments:

Post a Comment